3 minute read

Written by Andrew Flessa Leadership, Mindset, Blockchain, and Real Estate Expert

#multifamily #investment #economic #research

The multifamily national real estate market weathered the 2020 recession better than most property sectors—only industrial held up better. Heavy construction equipment used in earthmoving and building real estate have tripled in value since 2019.

Overall market deterioration was far less than in previous recessions, instead of deflation the net result we got was elevated inflation.

Still, it was a challenging year for multifamily as many owners lost rental income plus ancillary income from waived fees, deferred rents, and delinquencies.

There’s fierce competition for assets since liquidity is so plentiful because of Fed stimulus programs.

The industrial and multifamily sectors grew thanks to the abundance of the new domestic and foreign capital. The low-interest rate environment will persist and the resilience of real estate during slower economic times was proven once again to be true.

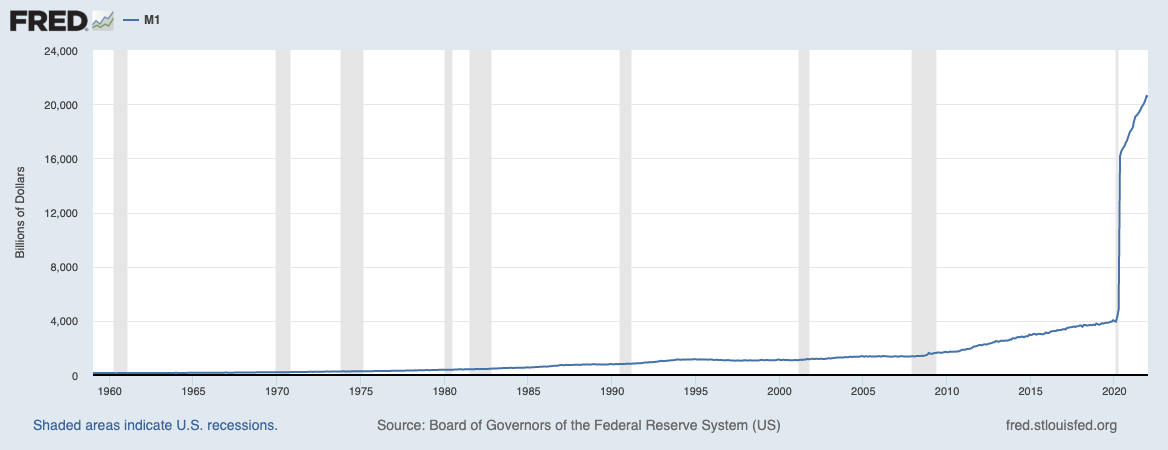

1. Trillions injected into the economy by the Fed

Here is the Fed’s main money supply measure, M1, from 1959 to now.

It’s a hockey stick graph. 35% of all the cash ever created was created in 2020.

2. America has gone through an urban to suburban shift

The pandemic induced recession impacted urban submarkets much more than suburban ones in 2020.

As a result, suburban submarkets will lead the multifamily sector’s growth in 2022 while urban submarkets will lag.

Five major pandemic related factors diminished the appeal of urban submarkets in 2020: remote working requirements, the closing of a portion of urban amenities, the reluctance to use public transit, a desire for more living space and a desire for greater access to the outdoors.

Non-pandemic related factors exacerbated the situation, including the high cost of urban apartments and shifting demographics.

Millennials are reaching life stages where urban living is often traded in for larger housing options in less-dense submarkets.

Urban submarkets will lag in the multifamily sector’s overall recovery.

Lower-density and less-expensive suburban submarkets held up remarkably well in 2020 and are positioned to lead overall market performance in 2022.

3. Multifamily as an attractive investment class

National multifamily occupancy rates are at record levels, with many apartment markets across the country seeing a strong increase in rents.

According to RealPage, an American multinational that provides property management software for the multifamily, commercial, single-family and vacation rental housing industries, nationwide effective asking rents have increased by 8.3%, the greatest gain since 2010. While rent growth may not be as robust going forward, demand for multifamily investments is predicted to remain strong in 2022.

Some of the best-performing multifamily markets between 2022 and 2023 include Boise, Phoenix, Worcester, Tucson, and Salt Lake City, with projected rent growth of 12% or more.

Northeast markets such as Philadelphia, Pittsburgh, and Hartford are predicted to see rent growth of 6% or less between now and 2023.

Additionally, Single-family housing remains in high demand

Residential real estate continues to see unprecedented growth that shows no signs of letting up.

Multifamily is still an asset class that is seeing solid returns and plenty of demand, but it’s the single-family space that’s really catching the eyes of investors. The single-family residential market in 2021 showed high demand but an inadequate supply of new development. This trend is expected to continue through 2030, as housing analysts calculate the current level of long-term under-building in a range from two to five million unbuilt homes.

Additionally, since most millennial adults today are still renters — they are playing catch-up in family and household formations — the demand curve for home ownership is vast for the next decade.

What has become clear is the pivotal opportunity for single-family property investment through 2030. Look for private equity and institutional investors to continue to deploy significant capital in the coming years to take advantage of the unmet demand for single-family housing.